Jan FOMC Preview - Is It Over Now?

Wednesday brings the January FOMC meeting where the Fed stays on hold for the 4th consecutive meeting as widely expected. The focus for markets lies in deciphering any signals about a potential rate cut in March, particularly following Fed officials’ pushback against the dovish sentiment that emerged after the December 15th meeting.

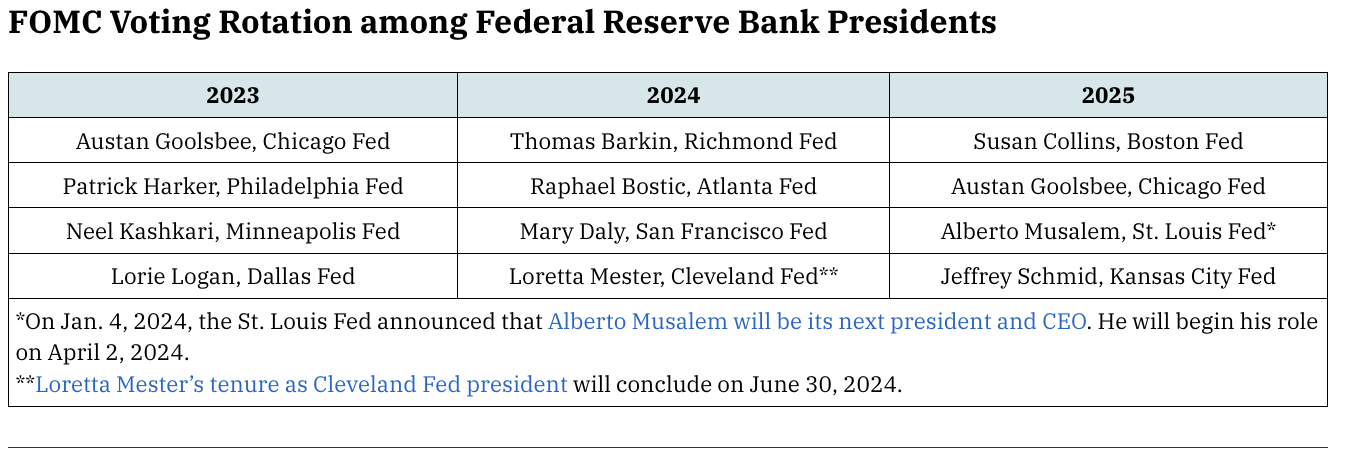

Voting Rotation 2024

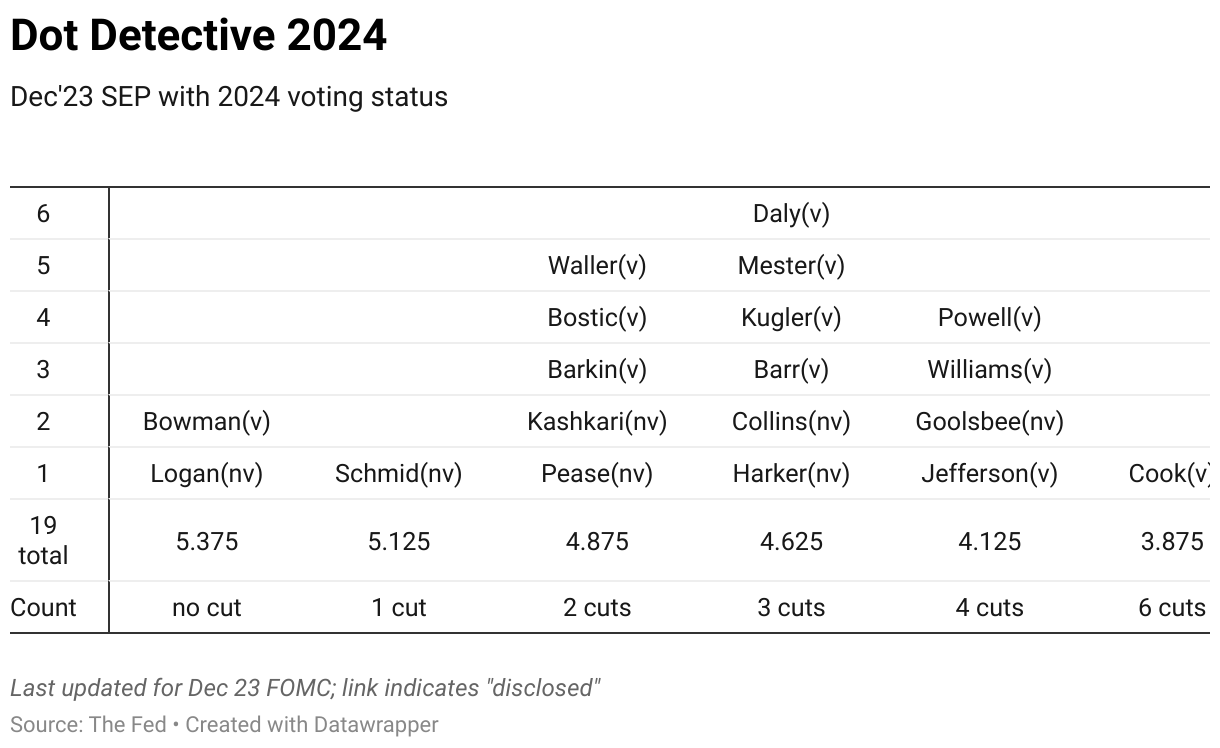

The January meeting introduces a shift in voting members, with Cleveland Fed President Mester (hawk), Richmond Fed President Barkin (hawk), Atlanta Fed President Bostic (dove), and San Francisco Fed President Daly (hawk) joining as new voters, replacing Logan (hawk), Harker (centralist to dove), Goolsbee (dove), and Kashkari (hawk). Also note that Mester’s impending retirement on June 30th, with the Cleveland Fed already searching for a successor. Should a replacement not be found in time, Chicago Fed President Goolsbee is poised to temporarily step in as a voter at the July meeting.

All four new voters have been publicly active recently and on net, they revealed a tendency towards a more hawkish stance.

Mester disclosed that she is a median dot but said “March is probably too early in my estimation for a rate decline”. She also put a bit more emphasis on inflation expectations and wage growth.

Daly is likely a median dot and has been advocating “gradualism” and “patience”. When asked about March, she pushed back with “I think it’s premature to think cut is around the corner”.

Barkin is likely one of the five 2 cut dots as he views inflation “a little stubborner”, but he has left the door open by saying that he won’t ”have any objection conceptually to toggling rates back toward normal levels as you build increasing conviction and confidence that inflation is on a convincing path back to target.”

Bostic forecasts only two rate cuts this year starting in Q3, but is open to adjust if “inflation comes down faster than his forecast”. Given these recent comments, Bostic seems to be more open-minded about moving his first cut forward, while the other three suggest an inclination towards delaying rate cuts.

Fedspeak Review

The views from this mix could well be the contour of the Jan meeting. The Fed is “in a good place”, with inflation coming down and labor market remaining healthy, thanks to the Beveridge curve. The Fed seems to have the luxury to truly “wait and see”.

Daly emphasizes patience, contingent on continued inflation reduction or “early signs that the labor market is starting to falter” to decide if “an adjustment is necessary”. Waller, however, in his last public appearance, instead of commenting on what would make him consider rates adjustment, chose to outline conditions for deferring rate cuts: stronger economic growth, a tighter labor market, and rebounding inflation. To me, they indicate different modal outlooks, but both highlight the risk of premature policy reversal, which could necessitate later rate hikes.

Daly: “So I’m going to be looking for two things. Do I get consistent evidence that inflation is coming down? Or do I get any early signs that the labor market is starting to falter? Neither one of those right now is pushing me to think that an adjustment is necessary, but we definitely want to keep our eyes on those things.”

Waller: ”Risks that would delay or dampen my expectation for cuts this year are that economic activity that seems to have moderated in the fourth quarter of 2023 does not play out; that the balance of supply and demand in the labor market, which improved over 2023, stops improving or reverses; and that the gains on moderating inflation evaporate.”

Indeed, the robust GDP growth in Q4 and strong spending could potentially pose challenges to the Fed’s confidence in decreasing inflation, but the Fed will receive the second estimate on Q4 GDP on Feb 28. The next piece of data the Fed is waiting for is the CPI annual revision on Feb 9, as we will get the seasonal factor update and relative value update at the same time before the release of Jan data on Feb 13. JPM’s Silver has previewed both revisions in his Focus pieces (Preview of the update to CPI seasonal factors, 01/11/24 and CPI relative importance changes unlikely to be major, 01/26/24). The conclusion here is quite straightforward: neither will change the broader inflation trends. Using the firm’s own SA models, for core inflation, there’s only “marginal upward revision” implied on net for the most recent three months.

Then there’s the labor market. Besides today’s slight-above consensus JOLTS number, consensus for Friday’s NFP of 175k is still well above the ~100k level needed to keep up with population growth. In terms of wage growth, with a 3%-3.5% target that the Fed seems as consistent with 2% inflation, Fed officials seem to be less concerned about the current level given the inflation progress. Specially Waller has said “at 4%, you’re a little high but you’re not that high. You can come down, but it’s not like when it’s 7-8% and productivity is 1.5%”.

The Fed probably wouldn’t want to close the door on a March cut, but it also has to be done in a way that won’t undo all the Fedspeak efforts bringing down March odds from as high as 80%. Therefore this meeting inevitably would have a seemingly more hawkish tone than what it should be, as there will be more time for the Fed to evaluate its policy stance before Humprey Hawkins in early March.

Jan Meeting Preview

Moving on to the specifics for tomorrow’s meeting. As this is going to be a meeting without SEP, all eyes are on statement language changes and Powell’s press conference.

Statement language: removing hawkish bias?

The street consensus here is the Fed will shift away from its current “hawkish bias” by removing “additional policy firming”. This anticipated change aligns with the growing comfort among Fed officials who believe that the current policy is sufficiently restrictive and we have reached the peak of the cycle.

There could be a slightly hawkish surprise, say if they replace it with something acknowledging that the policy rate will remain sufficiently restrictive until the Fed has confidence that inflation is coming down to 2%, as JPM’s Feroli suggested. In his latest piece, he also discussed in greater detail other potential language changes including growth, financial condition, and inflation outlook. Should this occur, I think Powell would soften this stance in the presser.

Guidance on March movement: will Powell push back on a March cut?

Consensus here is Powell is likely to leave the door open, adopting a meeting-by-meeting, data-dependent approach. Most economists think for the March decision, there’s likely not much to read from it. A hawkish surprise would be that Powell strongly suggests that the Fed is not considering a rate cut in March (similar to Mester). I think a more likely scenario is for the Fed to clarify its decision-making framework without any calendar guidance. A few different language plays could have a small hawkish or dovish tilt given historical context(I made some guesses..)

Instead of the timing of the first cut, perhaps we could gather more clues about the pace of the cutting cycle. There appears to be growing consensus among the members favoring a gradual, methodical pace, which is close to a pace of 25bp adjustment every other meeting. For me, the implication of such pace for the timing of the first cut is that a shallower path lowers the bar for an earlier insurance cut assuming the Fed is getting more sanguine about an eventual soft landing.

Balance sheet: hint at QT tapering announcement and timeline?

After the Dec meeting minutes as well as Dallas Fed President and former SOMA manager Lorie Logan’s speech on Jan 6, street strategists have written extensively about potential QT taper coming soon.

The expected timeline is similar: JPM suggested a March announcement, April start, and November stop (It’s all over now, QT, 01/12/24), Goldman suggested a May announcement/start and 2025Q1 stop (US Daily: An Earlier Start to Tapering, 01/10/24) and MS proposed a timeline of May announcement, June start and an early 2025 stop (Global Economics and Macro Strategy: Earlier Start, Slower Taper, 01/19/24).

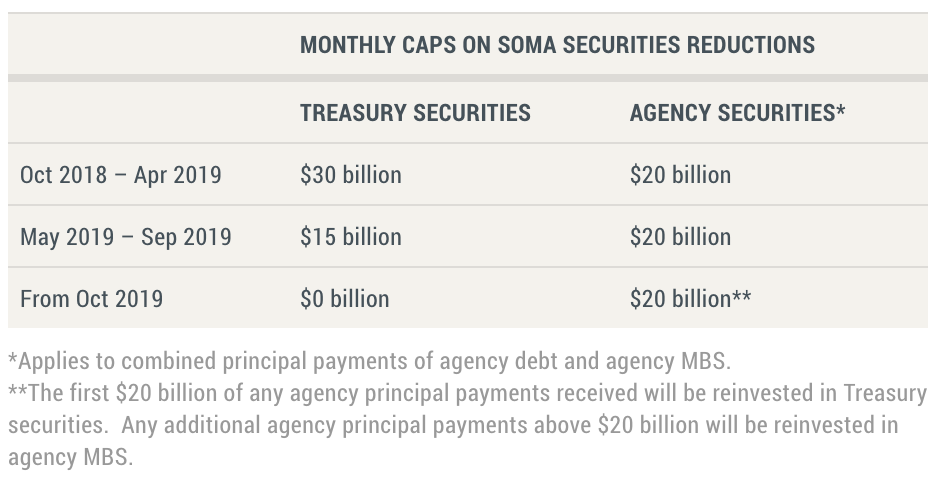

Most banks adopted the 2019 plan, cut the pace for Treasury from $60bn/month to $30bn/month but maintain the pace on MBS.

As for this week’s FOMC meeting, most strategists do not expect Powell to provide too many details in the presser, instead point to the Jan meeting minutes in Feb for more details. Recall in Dec meeting minutes, “several” participants suggested that “it would be appropriate for the Committee to begin to discuss the technical factors that would guide a decision to slow the pace of runoff well before such a decision.”

While this sounds like a preliminary discussion, Logan unsurprisingly was the most vocal on this one, suggesting that the Fed should taper QT when RRP “approaches a low level”. Waller, who has been early on QT and tapering back in 2021, also suggested that this should be a topic of discussion for the Fed this year. That said, unlike Logan, Waller seems to be comfortable with RPP going close to zero.

Beyond these two, there’s also a group of officials who are not rushing to taper yet, most notably Williams. These differences in Fed officials’ QT tapering expectations could mean QT tapering may be on the later/slower end of street estimates. It’s expected that we will keep getting clues in minutes from the Fed, but Powell’s response in the presser and whether it’s closer to Logan, Waller, or Williams will be critical for market participants to decide whether taper will start any time soon.

Recent Fed Quotes on QT

Logan (01/06) So, given the rapid decline of the ON RRP, I think it’s appropriate to consider the parameters that will guide a decision to slow the runoff of our assets. In my view, we should slow the pace of runoff as ON RRP balances approach a low level. Normalizing the balance sheet more slowly can actually help get to a more efficient balance sheet in the long run by smoothing redistribution and reducing the likelihood that we’d have to stop prematurely.

Bostic (01/08) Bostic also told reporters it’s an “open question” if and when the Fed should alter the pace at which it reduces its portfolio of assets, adding that the current pace is appropriate.

Williams (01/10) In its plans, the FOMC said that to ensure a smooth transition it intends to slow and then stop the decline in the size of the balance sheet when reserve balances are somewhat above the level it judges to be consistent with ample reserves. So far, we don’t seem to be close to that point. The decline in securities holdings has been absorbed almost entirely by a drop in the overnight reverse repurchase agreement facility (ON RRP). As a result, aggregate reserve balances are little changed from their levels in mid-2022, when balance sheet reduction started. Looking ahead to this year, as the balance sheet continues to shrink and usage of the ON RRP continues to decline, we will closely monitor money market conditions and the demand for reserves.

Goolsbee (01/11) Goolsbee said the Fed’s “autopilot” approach to the balance sheet reductions has served the Fed well, because investors understand the process and it does not need to be debated at each meeting. “We’ve got to have a high bar before we get off of it,” he said, adding that bank reserves are still abundant, meaning there is little risk for now that further reductions could disrupt financial markets. He said he would defer to Chair Jerome Powell about when to start conversations on slowing or halting those reductions.

Mester (01/11) Well, I can never say we shouldn’t be talking about some issue. Right. Because I think this is something that’s going to be coming up. John, I think rightly pointed out when he gave his remarks earlier this week that the balance sheet reduction is going as it’s been planned. And we did announce when we announced that started that in May of the plan in May 2022, that at some point as the balance sheet and reserves come down, we’re going to want to sort of reduce the pace of the reduction and normalize. But we still have a lot of reserves in the system, so we don’t have to do that imminently at all. I think there’s time and I’m sure this year will be when we start having the conversations of what that plan would look like and as we also committed to making sure that market participants in the public know what the plan is well before we implement it.

Waller (01/16) I would say sometime this year, it would be a reasonable thing to start thinking about it. I don’t think I’m speaking out of school, but it’s been coming close to two years since we first announced tapering, and I think when we did these numbers, it made sense that sometime in 2024, you would start thinking about tapering the pace to get back. Now, personally, I don’t think we need to taper the pace on MBS; we’re not even hitting the cap. So we don’t really need to keep MBS on my balance sheet as much, so I’m all in favor of letting those just continue to run off at the current pace. But Treasuries, we can start tapering that back and get reserves to where we want them. One other point to make, now everybody likes to go back to September 2019 and say all of a sudden you didn’t have enough reserves and there’s a bunch of kerfuffle in the financial markets. We have a standing repo facility now that we didn’t have in place. So if we start seeing reserves getting tighter and tighter, we may start seeing a lot of activity coming to the standing repo facility, and that’ll be a good signal for us that hey, we’re getting to that point. Again, that’s a tool we didn’t have back in 2019 that we do have now to help relieve kind of pressure on demand for reserves.

My guesses…

The below scenarios are what I think the market’s expecting… but I also marked my own base case. I could be way off, but I want to keep records of my thinking going into the meeting to reflect on afterwards.

(Jan 31st Update: Bold indicates what’s delivered. Author is grappling with how she got March wrong…)

Base Case

- Statement language to remove “additional policy firming…” and replace it with something close to “the Fed will keep policy rate restrictive until it’s fully convinced that inflation is coming down to 2%.” It could also take some of the language used in Jan 2019 when the Fed signaled pause: “In light of…. the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to…”

- March cut: Leave the door open without any commitment on either side. Need more data to confirm and the Fed will remain data-dependent.

- QT: Suggest we will see more details in the minutes and participants have started discussions on this topic. When asked about if QT is starting soon, only suggest “it’s natural to start the discussion this year” (close to Waller)

Hawkish Case

- Statement language keeps “additional policy firming…”

- March cut: similar to Mester and Daly, suggest it’s premature to consider rate cuts in March” / “March is too early for a cut”

- QT: Suggest that QT is running “as expected”, reserves abundant, there’s no urgency in altering the plan soon but closely monitoring progress (close to Williams)</span>

Dovish Case

- Statement language to remove “additional policy firming…” and replace it with something close to “act as appropriate” (Jun 2019)

- March cut: If asked about March, even if he’s not committing, not adding anything to push back expectations such as “March is not the focus of today’s discussion” or “today’s focus is still how long policy rate needs to stay restrictive” or even “if inflation comes high and we need to adjust policy, we will do so”

- QT: If asked about the recent decline in RRP, suggesting the Fed is closely monitoring and is discussing implications (close to Logan)